Editorial

White Paper

Why Enterprise AI Fails at Scale

Remember when AI was a line item in your "innovation budget," a curious experiment for the R&D folks? Those days are gone forever. Andreessen Horowitz's latest "16 Changes to AI in the Enterprise" of 100 CIOs across 15 industries report is a blaring siren: AI spending isn't just skyrocketing; it's shifting from speculative play to core, permanent budget lines.

If your enterprise still treats AI as a side project, you're not just behind; you're becoming irrelevant. The landscape has been remade in just a year. It's time for a brutal reality check.

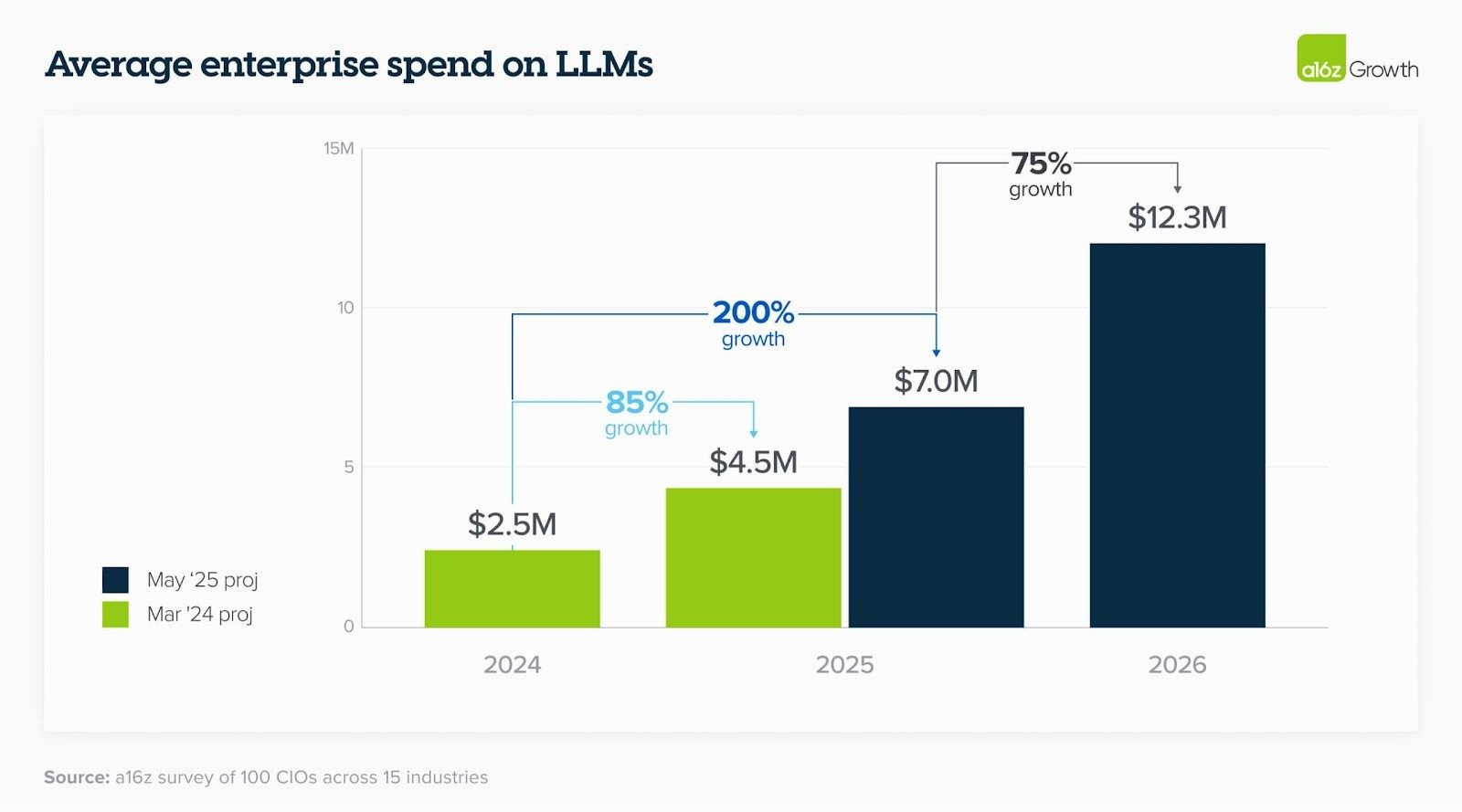

The numbers from A16Z are staggering. Enterprise leaders expect an average 75% growth in AI spend over the next year, and this isn't wishful thinking — it's driven by the discovery and implementation of new, valuable use cases. Internal applications were just the start; customer-facing GenAI is where the larger spending is now headed. This echoes what PWC found: a whopping 88% of organizations are increasing AI budgets due to agents, with many seeing 10%+ bumps.

This spending is graduating from innovation slush funds to permanent budget lines. Last year, innovation budgets covered ~25% of GenAI spending; now, it's a mere 7%. Reallocated central IT budgets (up to 39%) and business unit budgets (up to 27%) are now footing the bill. This isn't experimentation anymore; it's operationalization. It reflects a profound shift: organizations are no longer asking "if" AI, or even "if" agents, but are now deep in the "how," building infrastructure for an AI-driven future they see as inevitable.

Related Article: The Hidden Infrastructure Costs of Enterprise AI Adoption

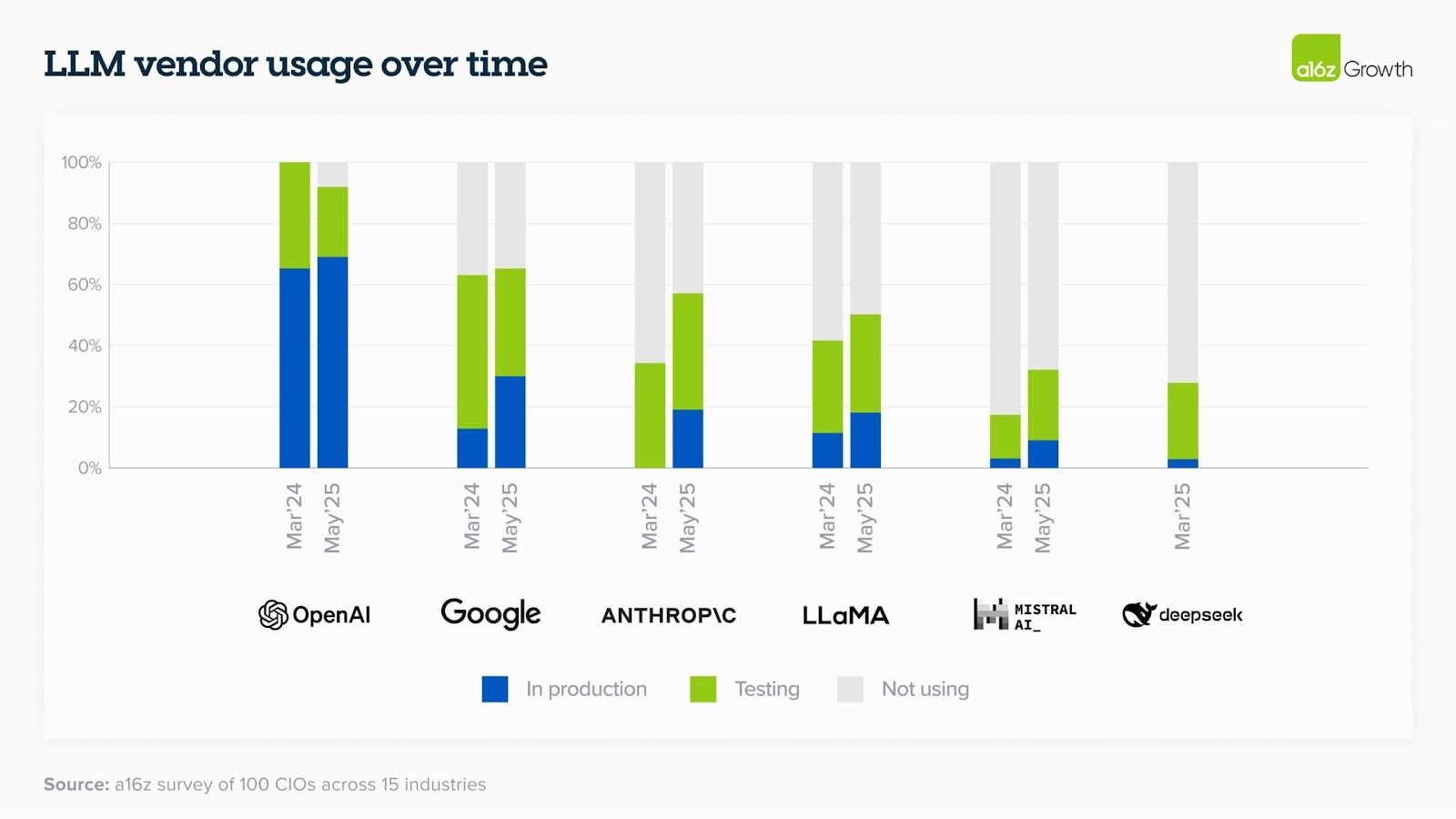

Forget the idea of enterprises locking into a single AI provider. A16Z reveals a surprising level of sophistication:

The way enterprises interact with and build upon AI models is also evolving rapidly:

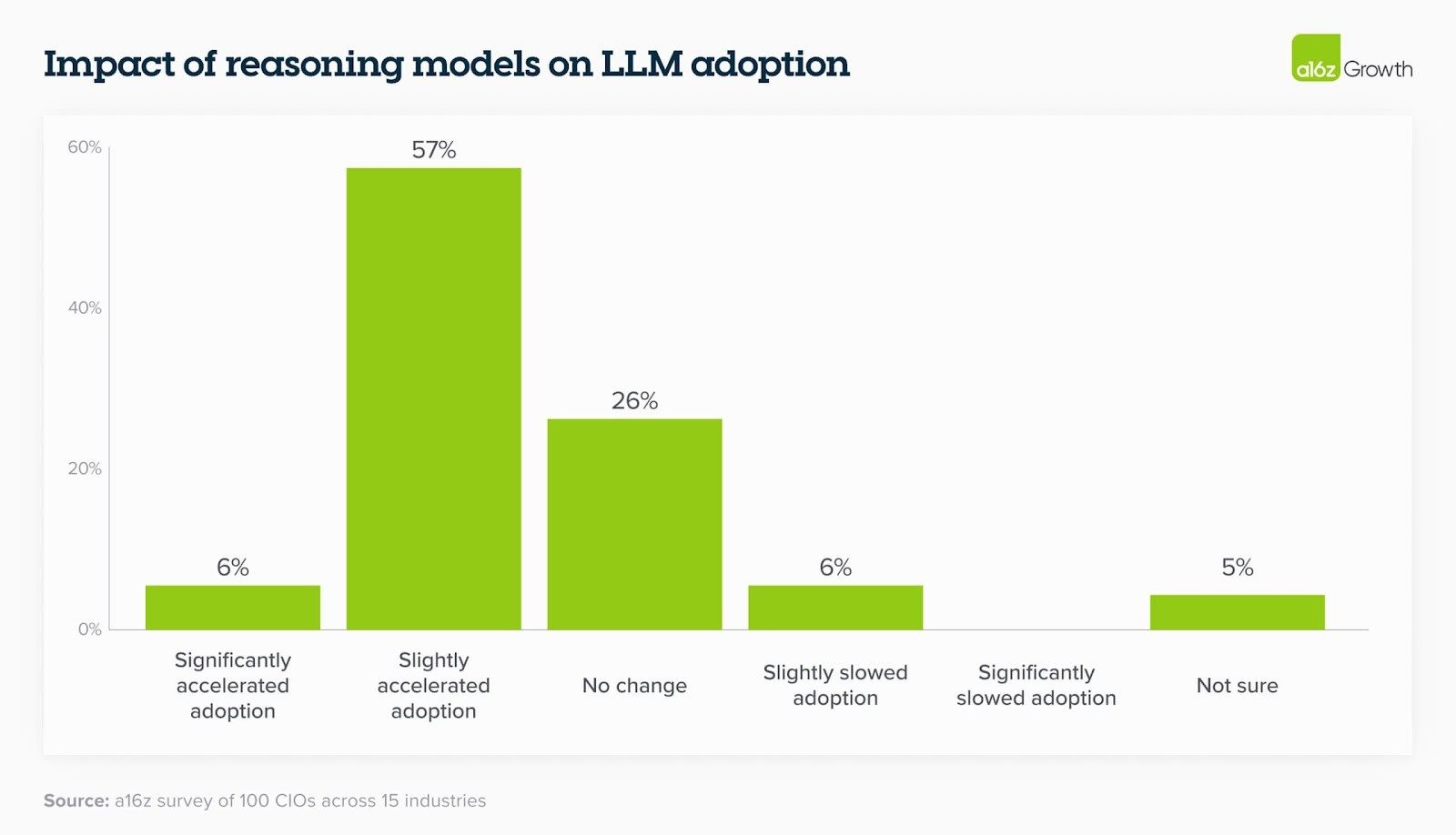

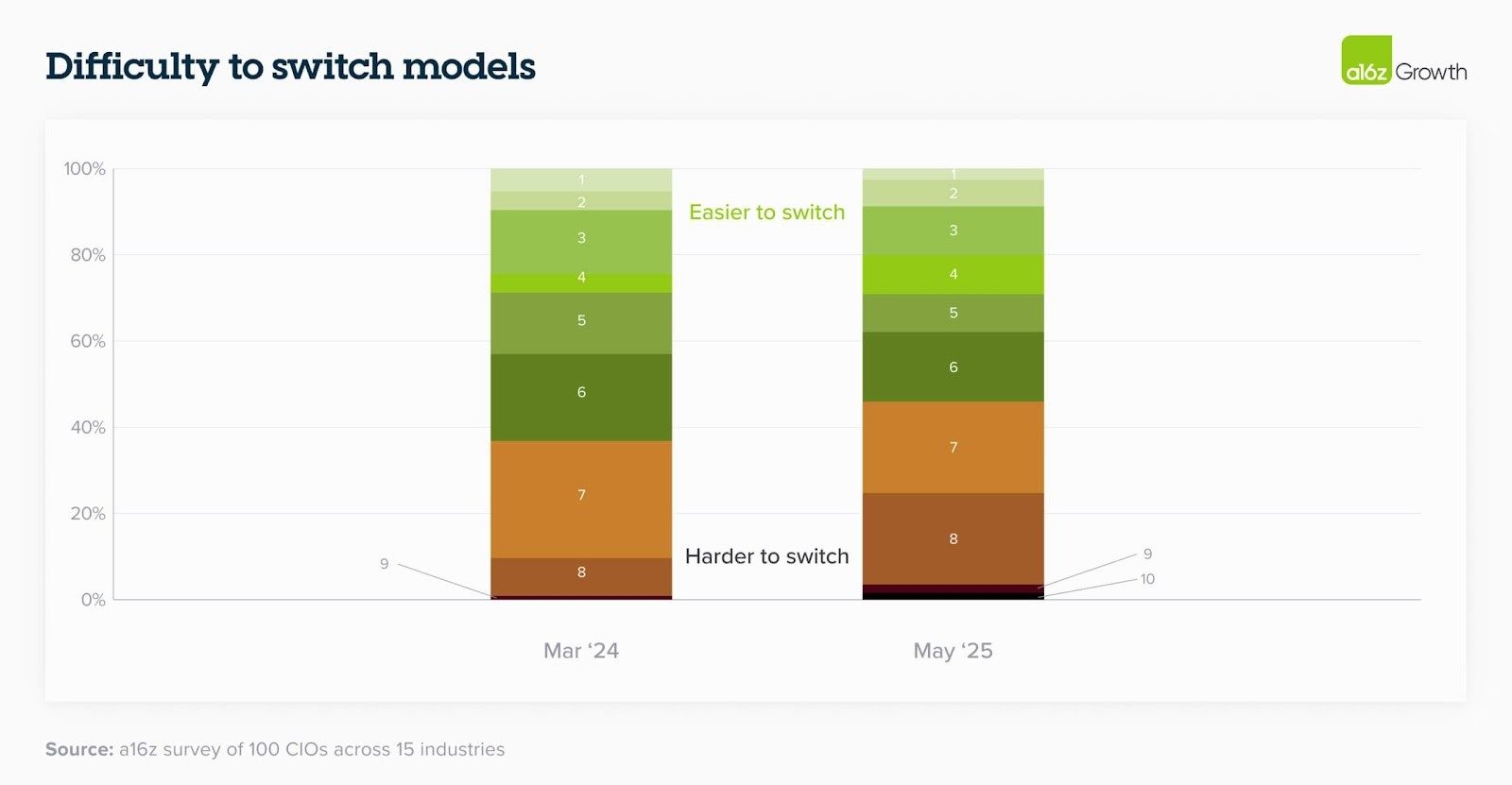

As AI moves from simple, one-shot tasks to complex, multi-step agentic workflows, a new form of lock-in emerges: switching costs are getting higher.

While enterprises initially designed for model interchangeability, the intricate dependencies in agentic systems make swapping out a core model a far more disruptive proposition. Every agent platform is now competing to capture a larger share of these interconnected use cases, knowing that interoperability, while desired, will be hard-won.

Last year, many enterprises were building their own AI solutions due to a lack of mature vertical applications. That's shifting. A16Z sees a "market shift towards buying third-party applications" as the ecosystem of AI apps matures. Vertical and functional agents are the hottest startup trend.

However, this isn't a simple swing. A fork is likely:

Related Article: AI Agents at Work: Inside Enterprise Deployments

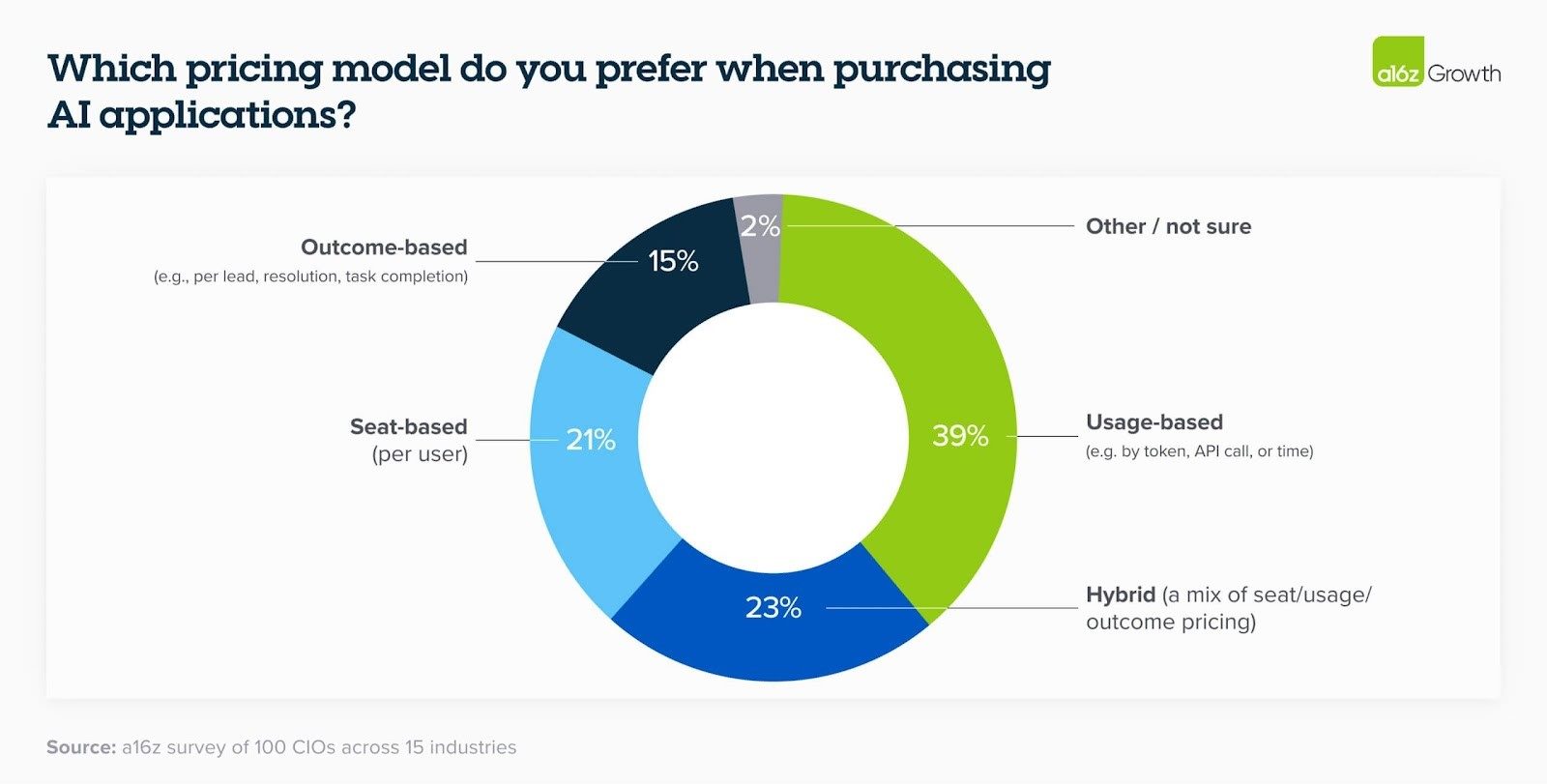

The old per-seat software model is struggling in the AI world. Outcome-based pricing is intriguing but fraught with challenges like unclear outcomes and unpredictable costs (only 15% of CIOs prefer it). Usage-based models (39% preference) seem to be a more comfortable interim solution.

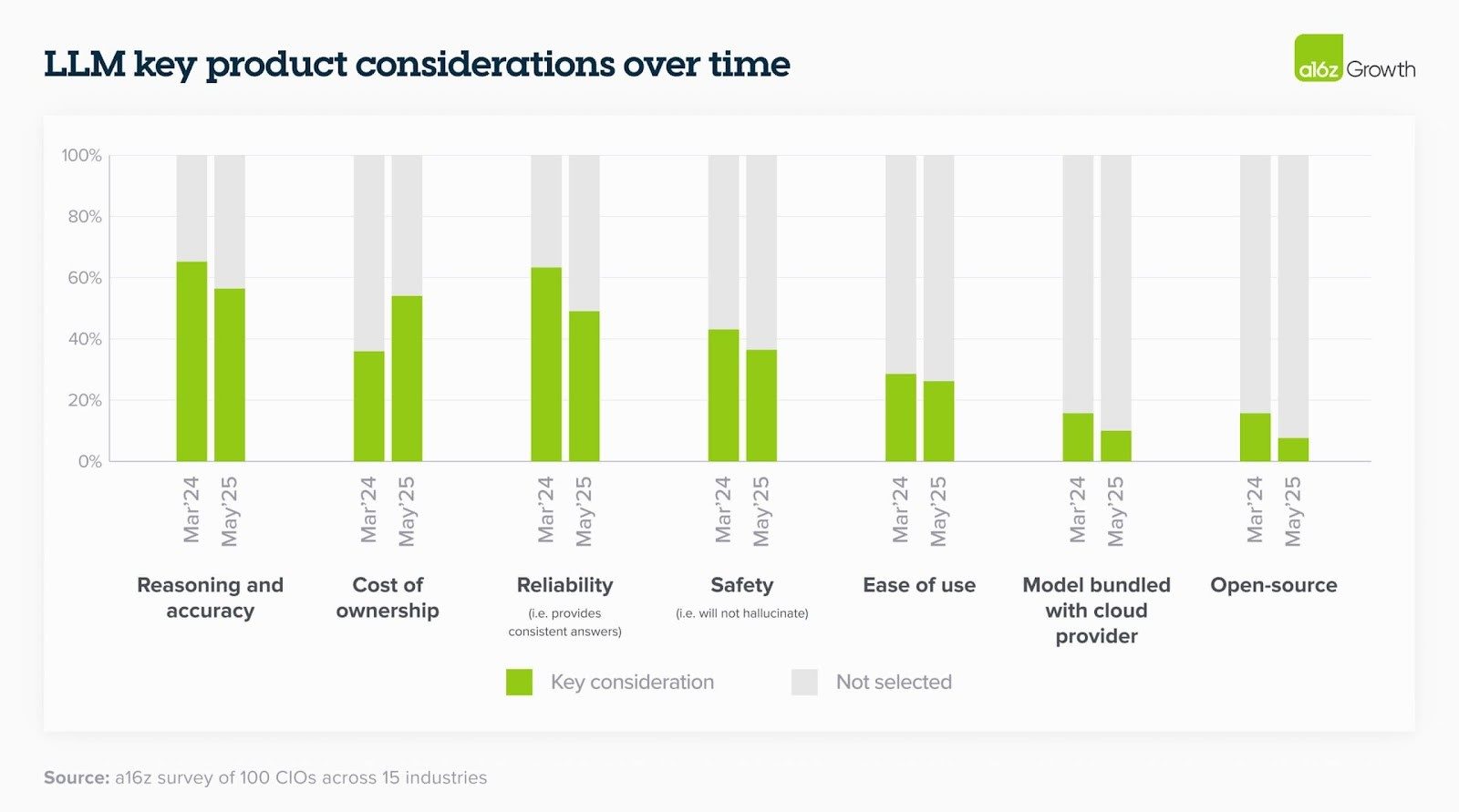

Meanwhile, some AI use cases are becoming table stakes (the baseline capabilities that are now required to compete effectively). Software development has seen a "step change," jumping from <40% to >70% of enterprises having it as an in-production use case in one year, driven by high-quality apps, increased model capabilities and no-brainer ROI. Enterprise search, data analysis and data labeling also saw big gains.

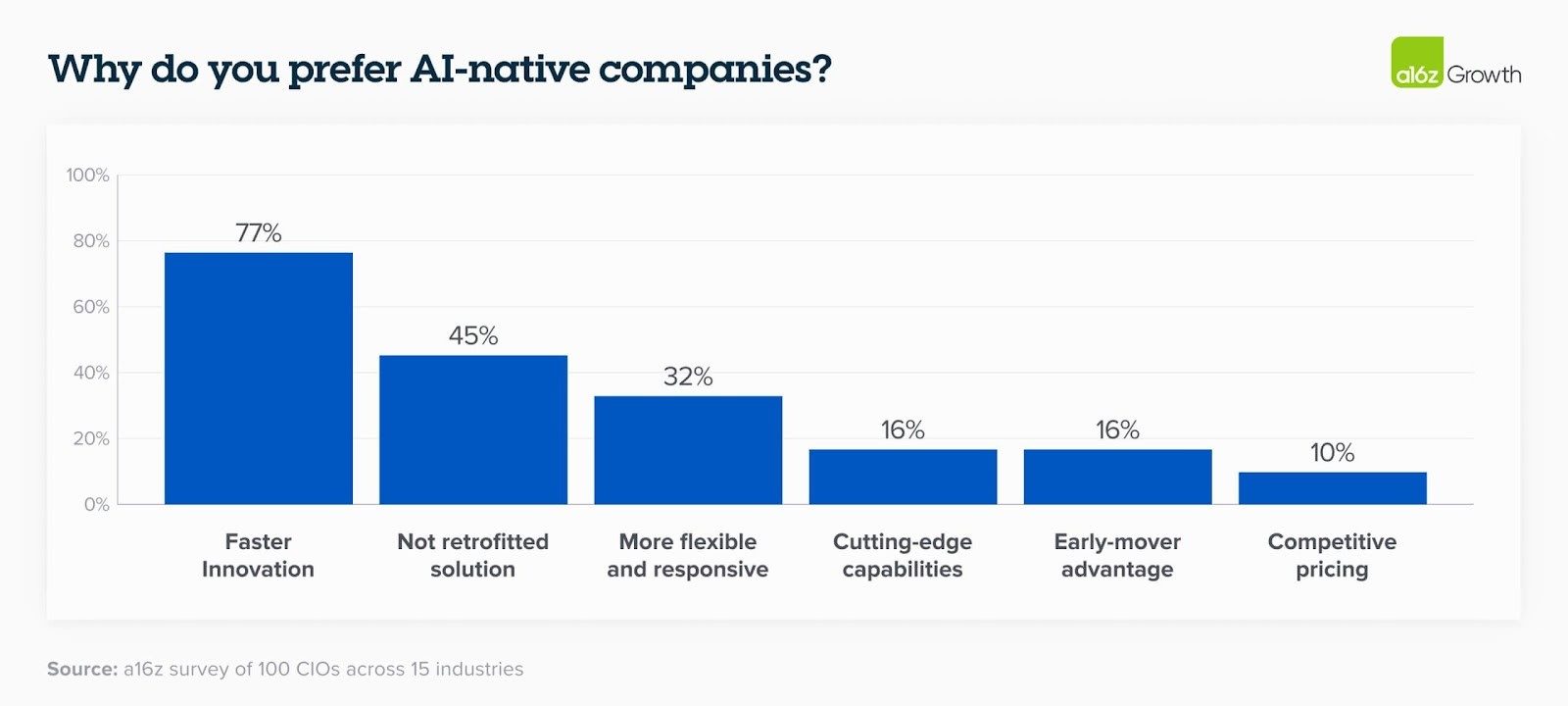

A year ago, incumbents (large tech providers, established enterprises) seemed to have a massive AI advantage: trust, distribution and capital. That advantage is now being challenged. A16Z's final, trend: AI-native quality and speed are starting to outpace incumbents.

Enterprises increasingly prioritize access to the best, state-of-the-art models as fast as possible. In areas like software development, the difference between first-gen AI coding assistants and new agentic coding platforms (Cursor vs. GitHub Copilot) is stark. Enterprises favoring AI-native companies cite their "faster pace of innovation" as the overwhelming reason. The old moats are eroding.

The overarching story from A16Z's 2025 enterprise AI report is one of relentless acceleration. Enterprises are adapting with surprising speed, mirroring consumer behavior in their multi-model adoption and demand for cutting-edge capabilities. This isn't just about adopting AI; it's about rewiring your organization to operate at AI speed. The shift to agents is not a distant future; it's ongoing and demands your immediate, strategic focus. If you're not already deeply engaged in understanding and implementing these changes, you're not just falling behind — you're risking being lapped by a future that has already arrived.

That data remains incredibly valuable for Retrieval-Augmented Generation (RAG) by providing specific context to off-the-shelf models through long context windows, and for internal benchmarking and validation of AI outputs.

Beyond direct licensing/usage fees, consider compute costs, data preparation/integration efforts, internal talent/training required, security/compliance overhead and the potential cost of errors or inaccurate outputs from less mature models.

Engage directly with internal tech leads/AI teams for tailored briefings, participate in executive AI workshops, follow curated industry analyses (like A16Z's) and encourage pilot projects that demonstrate these nuanced differences in real business problems.

Empower small, autonomous, cross-functional teams with direct access to state-of-the-art AI tools and clear mandates to rapidly prototype and iterate on high-impact AI use cases, shielding them from traditional bureaucratic hurdles.

Learn how you can join our contributor community.

Learn how you can join our contributor community.

Dr. David Priede, Ph. D., is the director of operations, advanced technologies and research at Biolife Health Center and is dedicated to catalyzing progress and fostering healthcare innovation. Connect with David Priede: