Editorial

Guide

Is AI Making Your Organization More Productive or More Dependent?

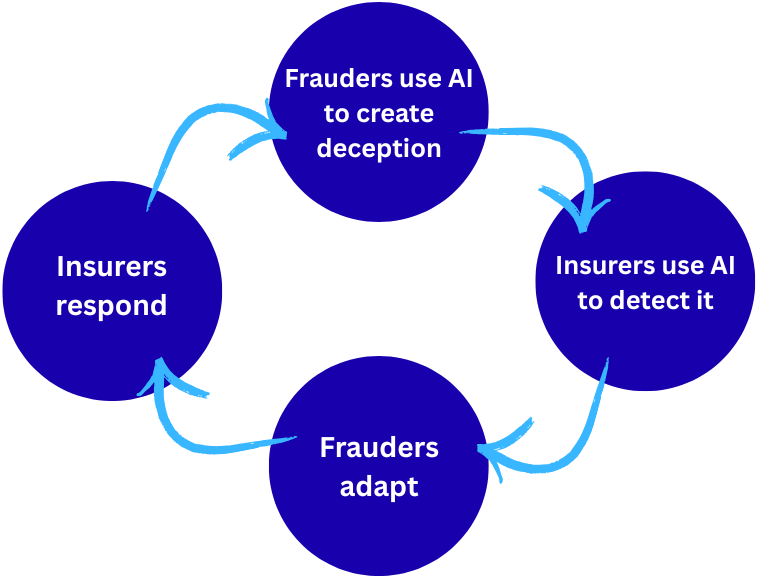

Artificial intelligence is changing insurance fraud from both directions at once.

On one side, AI is lowering the barrier to entry for fraudsters. Techniques that once required sophisticated technical skills can now be generated through AI, yielding convincing phishing emails, cloned voices, fabricated documents and synthetic identities in minutes.

On the other side, insurers are deploying many of the same technologies to detect fraud earlier, validate information faster and identify patterns that human investigators might never see.

The result is an escalating technological contest that increasingly resembles a cybersecurity battle more than a traditional claims investigation.

Insurance fraud has historically fallen into two categories: hard fraud and soft fraud.

AI amplifies both.

“AI is twofold,” said Katie Pope, senior vice president, executive lines, at The Liberty Company Insurance Brokers. “AI makes fraud much easier. But it also can stop some of the worst of it. On both sides of that, we are going to have to wait and see who wins in the end.”

Fraudsters can now create more convincing supporting evidence around otherwise weak claims. Fake invoices, manipulated photographs, generated correspondence and synthetic customer interactions are becoming easier to produce. The challenge is both detecting these fabricated claims and determining whether the evidence itself is authentic.

The most visible threat is generative AI-enabled social engineering.

Large language models can produce professional, contextual communications tailored to a target, meaning phishing campaigns no longer rely on poorly written emails full of spelling mistakes.

Voice cloning tools introduce another layer. A claims representative may receive a call that sounds authentic, meaning a policyholder verification workflow built around verbal confirmation suddenly becomes less reliable.

Document generation creates additional exposure. Fraudsters can produce repair estimates, medical paperwork and supporting documents at scale.

Identity fraud also becomes easier. Synthetic identities, which are combinations of real and fabricated information, can move through application workflows more effectively when paired with AI-generated artifacts.

Insurance has always been documentation intensive. AI changes the trust assumptions around that documentation.

And then there are “ghost agents.”

Ghost agents are fraudsters who pose as legitimate insurance agents or brokers, collecting premiums for policies that either do not exist or provide far less coverage than promised. They often target consumers through social media, text messages or unofficial websites, sometimes using stolen license information or fake credentials to appear legitimate.

In many cases, they sell policies that don’t ever exist, and they walk away with cash payments, supplying their victim with AI-generated fake documents. In the more pernicious cases, they apply for actual policies on the victim’s behalf and serve as the payment middleman. The ghost agent takes the payment on behalf of the client and then makes their own payment to the insurer. The ghost agent passes along the legitimate documents, only to close the policy shortly thereafter, pocketing the refund without the policyholder knowing.

In most cases, the policyholder doesn’t know they have been scammed until they get into an accident and realize they are left with absolutely no coverage.

Fraud opportunities exist across the entire insurance lifecycle.

It starts at the application stage. The application process increasingly faces synthetic identities, misrepresentation and fraudulent supporting documentation.

Insurers are responding with automated identity verification tools, document authentication and third-party validation. Application information is increasingly checked against external datasets using property records, vehicle databases, prior claims history, geospatial information and identity sources.

The goal is straightforward. Just like in the ‘80s, we trust, but verify.

But fraud does not stop after issuance. Behavior changes during the policy period often create fraud signals. Fraud is often telegraphed through sudden coverage increases before losses, geographic inconsistencies, unusual endorsement activity and asset changes inconsistent with prior records.

AI models are increasingly monitoring for these patterns continuously rather than relying on periodic review. "[Companies] are deploying next-generation AI to detect unusual behaviors and patterns that constitute an elevated risk of fraud,” said Patrick Foy, senior director, property and casualty strategic planning, at TransUnion.

Claims remain the highest-risk stage for fraud. Here, AI provides some of its strongest defensive value.

Machine learning systems can evaluate thousands of variables simultaneously, including shared repair facilities, geographic clustering, similar injury patterns, linked claim participants, historical claim relationships and timing anomalies.

Human investigators rarely have the bandwidth to detect these connections manually. AI becomes an early-warning system.

One of the more interesting developments is behavior analytics. Traditional fraud programs focus on what users submit. Behavior analytics examines how they submit it.

Insurers increasingly monitor signals such as typing speed and rhythm, copy-paste activity, navigation patterns, device fingerprints, session anomalies and multiple submissions from common environments. A legitimate claimant and a fraud ring often behave differently long before the claim itself is reviewed. These indicators do not prove fraud, but they do help prioritize investigations and improve triage.

All that said, insurance fraud strategy has long relied on two principles -— detect fraud, and deter fraud. AI strengthens both.

Winning fraud deterrence programs include strong identity verification, real-time validation, document authentication, behavioral monitoring and cross-referenced external data. The more friction introduced into fraudulent workflows, the lower the success rate. But technology alone is insufficient.

The temptation with AI is to assume better models automatically produce better outcomes. Insurance history suggests otherwise.

Successful fraud-fighting operations still depend on fundamentals, such as clean data, strong claims documentation, trained investigators, cross-functional workflows, consistent escalation procedures and human review and oversight.

Soft fraud illustrates the challenge.

Investigators may strongly suspect exaggeration while lacking sufficient evidence to prove intent. AI may identify patterns, but people still make decisions. Human expertise remains essential, especially as AI-generated evidence becomes more convincing.

The industry is entering a phase where fraud operations increasingly resemble adversarial AI systems.

This makes fraud less of a claims problem and more of an enterprise AI challenge touching underwriting, cybersecurity, identity management, customer experience and operations. The carriers most likely to succeed will be those that combine advanced analytics with strong operational discipline, third-party verification, identity controls and experienced investigators.

Because in fraud fighting, the winning strategy has not changed. Get the basics right. Verify everything. Use every available tool.

The difference now is that one of those tools can think at machine speed.

Learn how you can join our contributor community.

Learn how you can join our contributor community.