News Analysis

Guide

Is AI Making Your Organization More Productive or More Dependent?

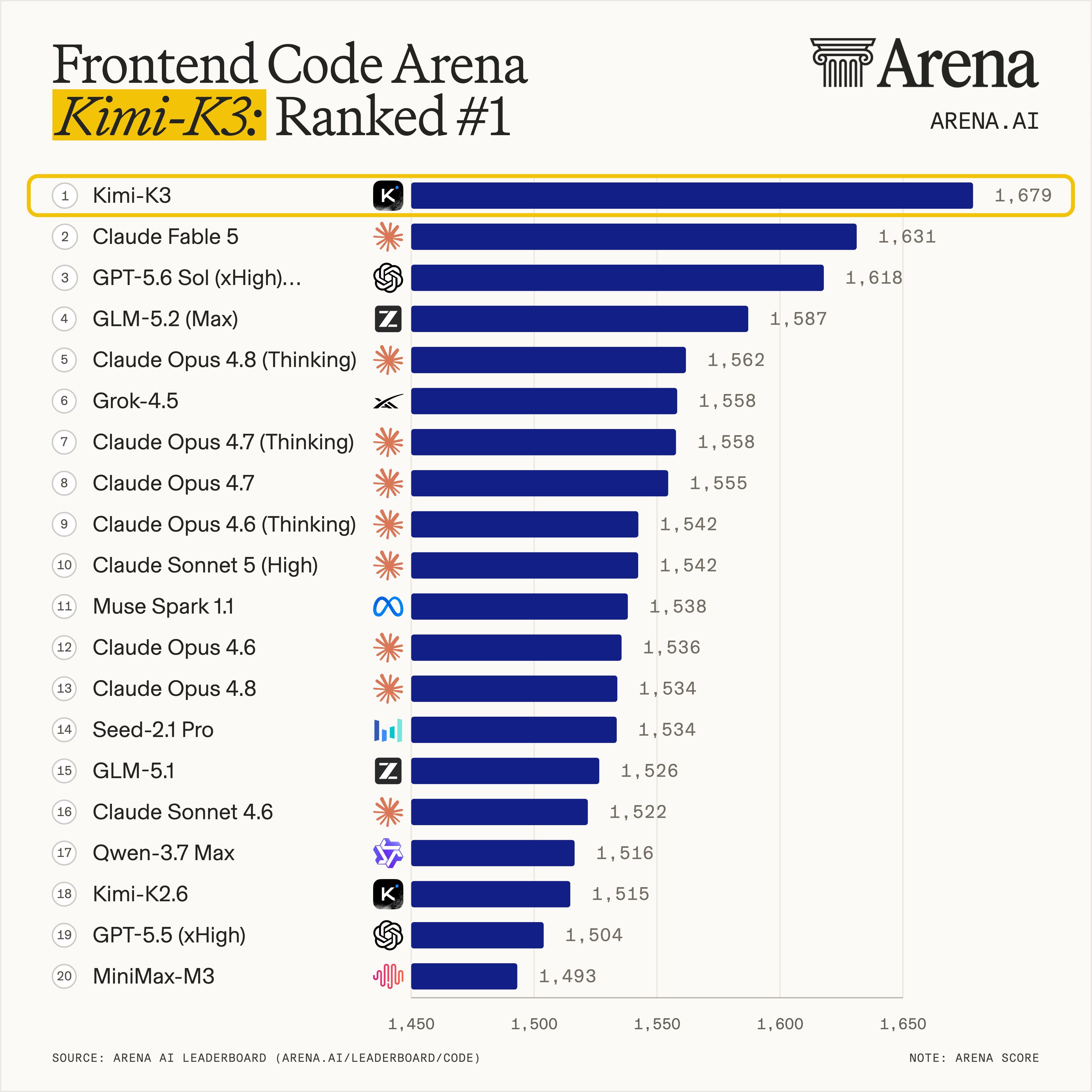

On July 16, 2026, Chinese AI lab Moonshot AI released Kimi K3 — a 2.8-trillion-parameter, open-weight model with a million-token context window and native vision. Within hours, it debuted at No. 1 on LMArena's frontend coding leaderboard, beating Claude Fable 5 in 76% of head-to-head matchups.

Independent testing by Artificial Analysis ranked it fourth globally with a score of 57.1, behind only Claude Fable 5 (59.9) and GPT-5.6 Sol (58.9).

The full model weights drop by July 27 under an MIT license. Anyone can download them and run them.

Kimi K3 introduces two architectural innovations — Kimi Delta Attention (KDA) and Attention Residuals — paired with a Stable LatentMoE framework that activates just 16 of 896 experts during inference. Moonshot AI says this delivers roughly 2.5x the scaling efficiency of its predecessor, Kimi K2, converting compute into capability more effectively.

In practical terms, K3 is purpose-built for long-horizon coding, agentic workflows and knowledge work. It can sustain multi-hour engineering tasks across large codebases with minimal human supervision, and its native visual understanding lets it incorporate screenshots, diagrams and runtime feedback into its reasoning.

The benchmark picture, drawn from both Moonshot's claims and independent evaluation, looks like this:

| Benchmark | Kimi K3 | Claude Fable 5 | GPT-5.6 Sol | Claude Opus 4.8 |

|---|---|---|---|---|

| Artificial Analysis Intelligence Index | 57.1 | 59.9 | 58.9 | 56.0 |

| Terminal-Bench 2.1 | 88.3% | 84.6% | 88.8% | 84.6% |

| GPQA Diamond | 93.5% | — | — | — |

| HLE (Humanity's Last Exam) | 44.3% | — | — | — |

| SciCode | 58.7% | — | — | — |

Moonshot itself acknowledges K3 still trails Fable 5 and GPT-5.6 Sol in overall user experience. But the gap is measured in single digits — and, critically, K3 is open-weight while those rivals are closed and proprietary.

Pricing tells the rest of the story. At $3 per million input tokens and $15 per million output tokens, K3 matches Anthropic's Sonnet 5 pricing tier and costs roughly half of what Opus 4.8 charges per task. Once the weights are public, self-hosted inference drops the cost further.

Kimi K3 is the latest in a pattern that's been accelerating for over a year.

Open-weight models from DeepSeek, Alibaba's Qwen, Meta's Llama and now Moonshot have narrowed the gap with proprietary systems to single digits on most benchmarks that matter to enterprise buyers.

Alibaba's Qwen alone crossed one billion downloads on Hugging Face in January 2026. The cost differential is clear-cut: self-hosted open models run at $1 to $5 per million tokens at scale, compared to $15–$60 for proprietary APIs.

As of mid-2026, Anthropic and OpenAI combined saw roughly $100 billion in annualized revenue. But they're arriving at that number through very different strategies, and the durability of those strategies is the real question investors need to answer.

Anthropic's bet is enterprise lock-in through developer tooling. Claude Code holds a reported 54% market share in AI programming tools, generating over $2.5 billion in annual revenue by itself.

Around 80% of Anthropic's revenue comes from business customers, with over 1,000 enterprises spending more than $1 million annually. The company's annualized revenue hit $30 billion by April 2026, and Sacra estimated it reached $47 billion by May.

Enterprise contracts carry higher retention, better expansion economics, and lower churn than consumer subscriptions. If any AI company has a path to sustainable margins, it looks more like this than like a consumer subscription business.

OpenAI's bet is consumer scale converting into enterprise revenue. ChatGPT commands roughly 900 million weekly active users, and the company says enterprise revenue has grown from 20% of the total in 2024 to 40% today, targeting parity with consumer by year-end.

But OpenAI is also projecting a $14 billion loss for 2026 and has committed to infrastructure spending that, even after being revised downward, runs to approximately $600 billion through 2030.

Both companies depend on proprietary model access as the core revenue driver. Every time an open-weight model closes the performance gap — as K3 just did — the premium enterprises are willing to pay for closed APIs narrows. The moat is not the model. The moat is the workflow, the integration, the data flywheel built around the model.

Anthropic's Claude Code ecosystem is an early example of that thesis. Whether it's enough to sustain premium pricing against open alternatives that keep improving every quarter remains an open question.

The financial pressure doesn't stop at the model labs. It flows downstream to the companies building the physical infrastructure those labs run on.

Oracle is a key example. The company's capital expenditure hit $55.7 billion in fiscal 2026, up from $21.2 billion the prior year, with guidance of $90–$95 billion for fiscal 2027. It's in the middle of a $250 billion data center expansion, fueled largely by debt rather than operating cash flow. That expansion is anchored by major commitments to OpenAI and Meta through projects like Stargate.

The stress is showing. On July 16 — the same day Kimi K3 launched — S&P Global Ratings cut Oracle's credit rating to BBB-, one notch above junk status. Moody's has a negative outlook, meaning further downgrades are possible. As DWS Americas head of fixed income George Catrambone noted, Oracle is "in a difficult spot" as credit conditions tighten.

Oracle's own SEC filing from late June paints a remarkably candid picture of the risks, including: customer credit exposure (i.e., AI labs not paying their bills), construction and permitting delays, GPU and power shortages and the possibility of stranded capacity if demand doesn't materialize. A Stargate expansion project in Texas was already canceled in March 2026 after financing negotiations stalled.

Oracle is funding its AI buildout through debt at a time when its biggest customers — OpenAI chief among them — are themselves unprofitable and heading into public markets to raise more capital. If model commoditization compresses the revenue those AI labs can generate, the downstream effect on infrastructure providers like Oracle is a credit risk that ratings agencies are already flagging.

Microsoft, Google and Amazon face similar capex exposure — combined spending projected above $400 billion in 2026 — but they fund it from operating cash flow, giving them a cushion Oracle doesn't have.

Claude Fable 5 and GPT-5.6 Sol still top the benchmarks, and enterprise buyers pay for reliability, support and integration, not just raw scores. But the trend line is unmistakable: the gap between open and closed is compressing on a quarterly cadence, and the price premium for closed access is harder to justify every time it does.

The questions that matter most moving forward:

The AI industry spent the last three years racing to build the most powerful models. The next three years will determine who can actually get paid for them.